2 Chapter 2 - Basics of Financial Analysis

2.1 Introduction

Financial Analysis focuses on selection, evaluation and interpretation of financial and market data of a firm usually contained in financial statements. Financial statements convey information about the operational performance and financial situation of an organization. Operational performance is related to how efficiently the firm is using its assets to produce return on its investments, while financial situation has to do with the firm’s capability to satisfy debt obligations on time. The main financial statements are a) balance sheet, b)income statement, and c) statement of cash flow.

The main type of financial analysis are:

• Financial ratio analysis

• Cash flow analysis

In this note I will focus on financial ratio analysis. Before reviewing financial ratios, we need to review the main financial statements.

In the next sections I first describe the main elements of the main financial statements. Then, I examine the different financial ratios.

2.2 Review of financial statements

Financial Analysis focuses on selection, evaluation and interpretation of financial and market data of a firm usually contained in financial statements. Financial statements convey information about the operational performance and financial situation of an organization. Operational performance is related to how efficiently the firm is using its assets to produce a return on its investments, while financial situation has to do with the firm’s capability to satisfy debt obligations on time. The main financial statements are a) balance sheet, b)income statement, and c) statement of cash flow.

2.2.1 Balance Sheet

The balance sheet is a statement that reports the book value of all firm assets along with all firm liabilities and shareholder equity. A firm asset is any resource the company acquires in order to operate and generate revenue and firm earnings. A firm liability is any payment commitment of the firm. A liability can be financial debt or accounts payable (e.g. when a firm acquires raw material and will do the corresponding payment later). Shareholder equity is the book value of a) the original amount of money invested by shareholders (common equity), and b) the cumulative retained firm earnings over time.

The most important equation in accounting is:

Total Assets = Total Liabilities + Shareholders’ equityIn other words, a firm can get resources (total assets) by either by getting money from shareholders or from its own operations (Shareholders’ equity), or by creditors such as financial institutions or suppliers (total liabilities).

For assets, liabilities and shareholders’ equity the firm must report different accounts. For example, asset accounts can be cash, accounts payable, inventory, gross plant and equiptment, etc. In the balance sheet a firm reports the book-value of each account, and this value represents the value of the account from the beginning of the firm until a certain date. Then, the balance sheet only has an ending period since the beginning period is always the first day when the firm started operations. Also, it is usually reported along with a comparable period one year ago.

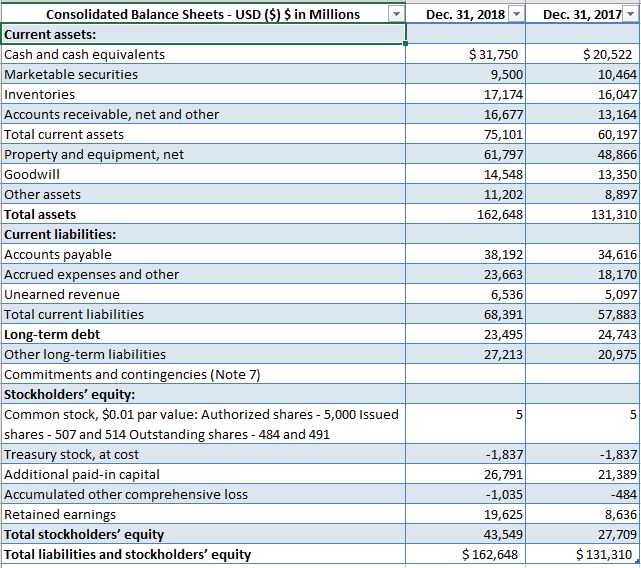

Below is the real balance sheet of Amazon for 2018. 1

We can see that Amazon total assets increased by about 24% in 2018 and total liabilities increased by about 15%.

We can see that Amazon total assets increased by about 24% in 2018 and total liabilities increased by about 15%.

2.3 Income statement

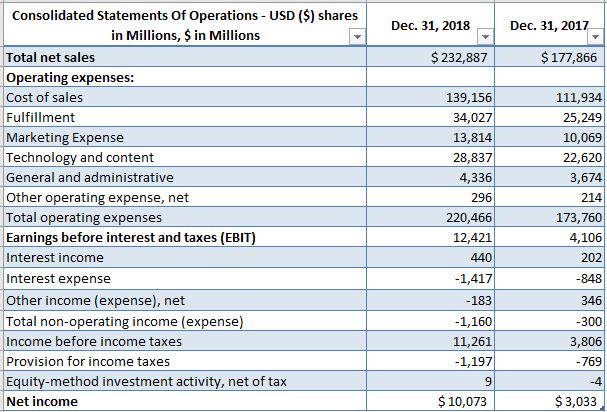

The income statement is like a picture of the productivity of a firm in a specific time period. Public firms must report financial statements each quarter (every 3 months), and also one annual report. In the income statement we can see how much the firm sold along with all type of expenses all the way until the net income of the period. Net income is the economic wealth generated in a period. Here is an example of the real Amazon 2018 income statement:

We can see that in 2018 Amazon significantly grew and also significantly increased net income. Sales increased by about 31%, while net income increased by about 232%, which is more than 3 times! This is an outstanding result for a big public firm.

We can see that in 2018 Amazon significantly grew and also significantly increased net income. Sales increased by about 31%, while net income increased by about 232%, which is more than 3 times! This is an outstanding result for a big public firm.

2.4 Cash flow statement

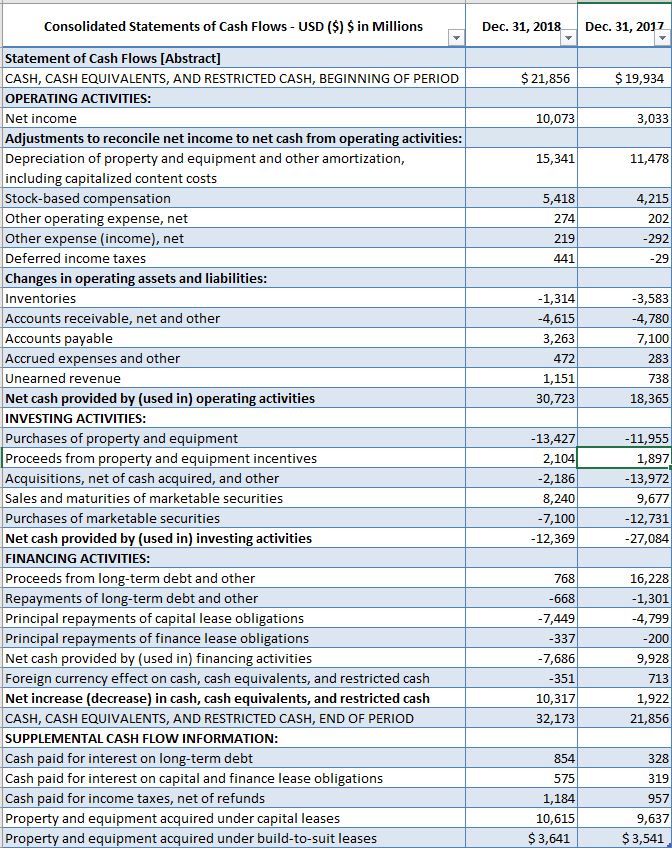

The cash flow statement shows how the firm generates cash flow from operation activities, financing activities and investment activities. Cash flow generation is different from net income due to accruals (e.g. accounts receivables, accounts payable) and due to other activities related to financing and investing. Here is the 2018 Amazon statement of cash flow:

We can see that Amazon significantly increased cash flow from operations by 67%, from $18,365 in 2017 to $30,723 in 2018.

2.5 Elements of Financial Statements

I will focus only on the basic elements of financial statements. This is not a comprehensive list of financial statement variables, but are the basic for computing the main financial ratios.

• Balance sheet variables:

– Assets:

∗ TA=Total assets

∗ CASH=Cash

∗ AR=Account receivables (also known as A/R)

∗ INV=Inventories

∗ CA= Current Assets

∗ GPEQ=Gross plant and equipment - these are the fixed assets of the company

∗ (ADEP)=Accumulated depreciation - this is a negative amount since depreciation conveys how much the fixed assets are being used and “exhausted”

– Liabilities and Shareholders’ Equity:

∗ TL=Total Liabilities

∗ AP=Account payable (also known as A/P)

∗ CL=Current liabilities included short-term debt

∗ LTD=Long-term debt

∗ CS=Common stock

∗ RE=Retained earnings

∗ SHE=Book value of Shareholder’s equity=CS+RE

• Income statement variables:

– S=Total Sales

– COGS=Cost of good sold

– SGAE=Sales and General Administrative expenses

– EBIT=Earnings before interest and taxes

– IE=Interests

– DEP = Depreciation of the period

– EBT=Earnings before taxes

– T=Taxes

– NI=Net income

– DIV=Preferred dividends payed

– RE=Retained earnings

I will do simple algebra to illustrate the relationship between the elements of the financial statements. The main equation of accounting is:

TA_{t}=TL_{t}+SHE_{t}

TA_{t} = Total assets, which is the book value of all resources the company owns at the end of period t.

TL_{t}=Total liabilities is the total value of debt (short-term and long-term debt plus current liabilities such as accounts payable).

SHE_{t} = book value of shareholders’ equity, which is the amount of capital investors have contributed to the firm -Common Stock (CS) and Preferred Stock (PS)- plus cumulative retained earnings (CRE):

SHE_{t}=CS_{t}+PS_{t}+CRE_{t} CS_{t}=Book value of common stock at period t

PS_{t}= Book value of preferred stock at period t

CRE_{t}= Cumulative retained earnings

Retained earnings of one period is equal to net income minus dividend payments in the period.

Then, the main three sources of firm’s resources are: a) TL: financing from creditors and suppliers, b) capital from investors (CS and PS), and c) retained earnings (cumulative net profits from business operations minus dividends) (CRE):

TA_{t}=TL_{t}+(CS_{t}+PS_{t})+CRE_{t}

CRE_{t}=CRE_{t-1}+RE_{t}

RE_{t}=NI_{t}-DIV_{t}

Now, looking closer to both Total Assets and Total Liabilities, we can see that:

TA_{t}=CA_{t}+NFA_{t}

NFA_{t}=GPEQ_{t}-ADEP_{t}

CA_{t}=CASH_{t}+AR_{t}+INV_{t}

TL_{t}=CL_{t}+LTD_{t}

Now, let’s analyze in detail the relationship of the income statement variables:

EBIT_{t}=S_{t}-COGS_{t}-SGAE_{t}-DEP_{t}

DEP_{t} represents the depreciation of assets and amortization of non-tangible assets at the end of period t. Depreciation refers to the amount of the assets that is used or exhosted in the period, so it is considered a “non-cash” expense to calculate earnings.

EBT_{t}=EBIT_{t}-IE_{t}

NI_{t}=EBIT_{t}-IE_{t}-T_{t}

Plugging the formula of EBIT:

NI_{t}=S_{t}-COGS_{t}-SGAE_{t}-DEP_{t}-IE_{t}-T_{t}

Then, Net Income is equal to sales minus cost of good sold (variable costs) minus sales and general administrative expenses (fixed costs) minus depreciation minus interest expenses and minus tax expenses.

At the end of each year, if the firm generated positive net income, firms have to decide whether to pay dividends to shareholders or wait for future periods. The dividends are payed from the net income generated in the period. Then, with the net income the firm pays dividends, and whatever is left is reinvested in the firm. This amount reinvested to the firm is called retained earnings. Retained earnings at the end of a period is added to cumulative retained earnings, which is part of shareholders’ equity. Then, we can see that the way income statement and balance sheet are connected is through net income:

TA_{t}=TL_{t}+(CS_{t}+PS_{t})+CRE_{t}

CRE_{t}=CRE_{t-1}+RE_{t}

RE_{t}=NI_{t}-DIV_{t}

TA_{t}=TL_{t}+(CS_{t}+PS_{t})+CRE_{t-1}+NI_{t}-DIV_{t}

We can conceptualize a firm as an engine with the potential to generate economic wealth measured in future cash flows. These cash flows must be able to satisfy:

• The required rate of return of the firm shareholders, and

• The debt rate of creditors

In other words, after a period, the firm must be able to generate wealth from its operations to first cover the financial debt with creditors, and then, the expected dividends (or return) that shareholders require. However, before paying creditors and shareholders, the firm also has to reserve cash flows to invest in fixed assets in order to expand or grow, and also it has to reserve some resources for working capital for the following period.

Working capital refers to the short-term liquidity and operational efficiency. Working capital is the difference between current assets and current liabilities. Then, we can visualize the different cash flows generated by a firm in a period as follows:

Cash flow from operations MINUS Cash flow invested in working capital MINUS Cash flow invested in capital expenditure MUST BE EQUAL to Cash flow required by creditors + Cash flow required by shareholders.

This is also called “cash flow identity”.

In the following section I further decompose the elements of total assets to identify these types of cash flows and verify why this is true.

2.6 Cash flow identity

I will examine in detail the main equation of accounting to identify all different types of cash flows generated by the firm. To keep the analysis simple, I will assume that the total revenue of the firm comes from the core business operations and not from other activities such as financing or investing activities. I start with the main accounting equation:

TA_{t}=TL_{t}+SHE_{t}

Total assets, total liabilities and shareholders’ equity are as follows:

TA_{t}=CA_{t}+NFA_{t}

TL_{t}=CL_{t}+LTD_{t} SHE_{t}=CS_{t}+PS_{t}+CRE_{t}

Decomposing CRE_{t} in more detail:

CRE_{t}=CRE_{t-1}+RE_{t}

RE_{t}=(NI_{t}-DIV_{t})

Then I can express the main accounting equation as:

CA_{t}+NFA_{t}=\left[CL_{t}+LTD_{t}\right]+\left[CS_{t}+PS_{t}+CRE_{t}\right]

Now I can subtract the same figures but from the previous accounting period in order to get changes for each amount:

\left(CA_{t}+NFA_{t}=\left[CL_{t}+LTD_{t}\right]+\left[CS_{t}+PS_{t}+CRE_{t}\right]\right)-\left(CA_{t-1}+NFA_{t-1}=\left[CL_{t-1}+LTD_{t-1}\right]+\left[CS_{t-1}+PS_{t-1}+CRE_{t-1}\right]\right) Then, I get:

\left(\Delta CA+\Delta NFA=\left[\Delta CL+\Delta LTD\right]+\left[\Delta CS+\Delta PS+\Delta CRE\right]\right)

The chage of cumulative retained earnings (CRE) is actually equal to retained earnings of the period t:

CRE_{t}=CRE_{t-1}+RE_{t}

CRE_{t}-CRE_{t-1}=RE_{t}

\Delta CRE=RE_{t}

Retained earnings is actually net income minus dividen payment:

\Delta CRE=(NI_{t}-DIV_{t})

Net income comes from sales and all expenses:

NI_{t}=EBIT_{t}-IE_{t}-T_{t}

EBIT_{t}=S_{t}-COGS_{t}-SGAE_{t}-DEP_{t}

NI_{t}=S_{t}-COGS_{t}-SGAE_{t}-DEP_{t}-IE_{t}-T_{t}

Plugging equations (4) and (5) in equation (3):

\Delta CA+\Delta NFA=\left[\Delta CL+\Delta LTD\right]+\left[\Delta CS+\Delta PS+(S_{t}-COGS_{t}-SGAE_{t}-DEP_{t}-IE_{t}-T_{t}-DIV_{t})\right]

I move the terms of this equation by cash flow type:

\left[IE_{t}-\Delta LTD\right]+\left[DIV_{t}-(\Delta CS+\Delta PS)\right]=\left[(S_{t}-COGS_{t}-SGAE_{t}-T_{t})\right]-\left[\Delta CA-\Delta CL\right]-\left[\Delta NFA+DEP_{t}\right]

I grouped the terms as follows:

Cash flow to creditors = \left[IE_{t}-\Delta LTD\right]

Cash flow to shareholders = \left[DIV_{t}-(\Delta CS+\Delta PS)\right]

Cash flow from operations = \left[(S_{t}-COGS_{t}-SGAE_{t}-T_{t})\right]

Cash flow allocated to net working capital = \left[\Delta CA-\Delta CL\right]

Cash flow invested in capital expenditure = \left[\Delta NFA+DEP_{t}\right]

Then, according to equation __, we conclude that:

Cash flow to creditors + cash flow to shareholders = cash flow from operations - cash flow for net working capital - cash flow for capital expenditure

Doing this detailed analysis of financial statement items we can conclude that creditors and shareholders can claim cash flow from operations AFTER the firm invest in both working capital for the short term and capital expenditure needed for the firm to stay in business. This makes sense and it is actually the foundations of the concept free cash flow.

2.7 Financial ratio analysis

A ratio is basically a division between two numbers. A ratio conveys information about the relationship between two variables. A financial ratio can be any division between two variables from the financial statements. We can classify financial ratios in the following groups:

• Profitability

• Return on investment

• Financial leverage

• Liquidity

• Activity

Besides these set of financial ratios, other simple ratios to evaluate the company’s operating performance and financial condition is to express financial statements in terms of percentages. For example, in the case of the balance sheet, all items can be expressed in terms of percentage of total assets; in the case of the income statement, all items can be expressed in percentages of total sales. These financial statement are also known as “Common-size” financial statements, or “Common-size” analysis.

2.8 Return on Investment and profitability Ratios

Now let’s play with these variables to create financial ratios that convey information about return on investment. If I were one of the main investors of a firm, I would like to see how productive the firm is utilizing its assets, and then, how much I would make from my investment. Then, I would be interested in the following ratios:

ROA_{t}=\frac{NI_{t}}{TA_{t-1}}

ROABIT_{t}=\frac{EBIT_{t}}{TA_{t-1}}

Note: the use of t-1 is optional and it depends on the specific analysis. Many analysts compute ROA of t using assets of the previous period (t-1). ROA and ROABIT are measures of return on assets. In other words, both convey information about what percentage represents earnings with respect to the total book value of its assets. ROABIT is also known as “Basic earnings power”. The decision about which of these two measures is the best to represent return on assets depends on the specific context and also specific information to be analyzed.

A simple measure of operational efficiency is asset turnover (ATO), which is how often or how fast the assets of the firm are generating revenues:

ATO_{t}=\frac{S_{t}}{TA_{t-1}}

Learning about the ROA can give investors an idea about how efficient the company is using its assets. However, if an investor observes an increase of ROA from one year to another, he or she will not know what is the source of this improvement. ROA can change due to changes in profit margin or asset efficiency. Let’s do simple math to identify two components of ROA. If we multiply the ROA components by the ratio S/S, which is equal to one:

ROA_{t}=\frac{NI_{t}}{TA_{t-1}}=\frac{NI_{t}}{S_{t}}*\frac{S_{t}}{TA_{t-1}}

Now we get 2 components of ROA, that is Profit Margin and Asset Turnover.

\frac{NI_{t}}{S_{t}}=Profit\,Margin

\frac{S_{t}}{TA_{t-1}}=Asset\,Turnover

Then we can say that ROA=(Profit margin)*(Asset turnover). This is the main derivation of the “Du Pont” System since Du Pont Corporation developed this simple but very useful method to decompose financial ratios.

The Net Profit margin is a percentage of the sales that actual profits represent. Let’s provide the following example to see the application of the ROA decomposition. If last year ROA was 0.20 and this year was 0.10, I will be interested in knowing the main reason of this decline. The sources of this decline can be due to a) reduction in operational efficiency, b) decrease in sales and increase in costs, c) increase of total assets. Then, with the decomposition of ROA investors can see in detail the source of this decline.

Another important ratio for investors is the return on equity - maybe the most important for them. ROE is simply:

ROE_{t}=\frac{NI_{t}}{SHE_{t}}

Now let’s play with EBIT instead of NI in order to see in more detail the role of financing (IE) and taxes (T) in the bottom line of the business, which is Earnings. Defining ROA before interests as:

ROABI_{t}=\frac{EBIT_{t}}{TA_{t-1}}

Doing simple math with the ratios and the income statement rules:

NI_{t}=EBIT_{t}-IE_{t}-T_{t}

If we consider a Tax Rate TR, then we can express NI as:

NI_{t}=\left(EBIT_{t}-IE_{t}\right)\left(1-TR_{t}\right)

T_{t}=\left(TR_{t}\right)\left(EBIT_{t}-IE_{t}\right)

Then:

NI_{t}=EBIT_{t}-\left(EBIT_{t}\right)\left(TR_{t}\right)-IE_{t}+\left(IE_{t}\right)\left(TR_{t}\right)

Factoring EBIT:

NI_{t}=\left[\left(EBIT_{t}\right)\left(1-TR_{t}\right)\right]-IE_{t}+\left(IE_{t}\right)\left(TR_{t}\right)

\left(EBIT_{t}\right)\left(1-TR_{t}\right)is a version of “unleveraged” earnings. I will name it “unleveraged net income”, since this amount would be earnings after taxes in the case of no financing from debt. Without debt, interest expenses are zero. The term \left(IE_{t}\right)\left(TR_{t}\right) is positive in the formula, meaning that it is adding value to Net Income. This term represents a benefit of getting debt to finance the firm. I will call this term “Tax benefit”

Then, continuing playing with the decomposition of Net Income:

NI_{t}=UnleveragedNI_{t}-IE_{t}+TaxBenefit_{t}

Then, the firm get benefits from financing from debt, besides the benefit of investing more money in productive activities of the firm. Remember that total resources of a firm (assets) is equal to the sum of shareholders’ equity and total liabilities. Both long-term debt and short-term debt are part of liabilities, so both can increase the total resources of a firm, which are used to make earnings.

Obviously, interest expenses also has a negative effect on Net Income as we can see in the formula. However, many times this IE is less costly than the cost of capital using owners’ equity. In other words, the firm has to find ways of producing much more than the amount of IE when investing the amount of the debt in the firm (this happens when the interest rates are less than the discount rate of firm’s cash flows).

Most of the time firms end up asking for debt simply because they do not have enough cash to start or continue operations. However, entrepreneurs have to be aware that getting debt has its own benefits in terms of tax benefits, and also in terms of opportunity cost. In other words, if I am an entrepreneur and had enough cash to launch my company, then I have to consider getting financing from debt in case I can get access to a descent interest rate (unfortunately, it is too hard to find this in the Mexican Banking industry!). Even with high interest rates, I could help my company grow faster and take advantage of specific market opportunities if I believe that my business idea has potential.

Now, I continue playing with return on investment ratios to examine the components of earnings:

ROA_{t}=\frac{\left(EBIT_{t}-IE_{t}\right)\left(1-TR_{t}\right)}{TA_{t-1}}

Now I can decompose ROA again to identify the NI share of owners’ equity. Multiplying the ROA numerator by EBIT and dividing by EBIT:

ROA_{t}=\left[\frac{\left(EBIT_{t}-IE_{t}\right)\left(1-TR_{t}\right)}{EBIT_{t}}\right]\left[\frac{EBIT_{t}}{TA_{t-1}}\right]

I can identify two components or share of Net Income: owners’ equity share and creditors’ share:

\frac{EBIT_{t}-IE_{t}}{EBIT_{t}}=NIShEq_{t}= Net income share of owners' equity

\frac{IE_{t}}{EBIT_{t}}=NICrEq_{t}=Net income share of creditors

Then, I have:

ROA_{t}=NIShEq_{t}\left(1-TR_{t}\right)\left(ROABIT_{t}\right)

Then, we can say that ROA can also be expressed as Net Income share of owners’ equity after taxes times ROA Before Interest and Taxes. Now we can decompose the second factor multiplying and dividing by Sales in order to identify operating margin and asset turnover:

ROA_{t}=\left[\frac{\left(EBIT_{t}-IE_{t}\right)\left(1-TR_{t}\right)}{EBIT_{t}}\right]\left[\frac{EBIT_{t}}{TA_{t-1}}\right]

ROA_{t}=NIShEq_{t}\left(1-TR_{t}\right)\left(\frac{EBIT_{t}}{S_{t}}\right)\left(\frac{S_{t}}{TA_{t-1}}\right)

Then we can say that ROA is equal to Net Income share of ownners’ equity after taxes times Operating Margin times Asset Turnover:

ROA_{t}=NIShEq_{t}\left(1-TR_{t}\right)\left(OperatingMargin_{t}\right)\left(AssetTurnover_{t}\right)

Unlike Profit Margin, Operating Margin is a percentage of sales that the firm is generating as earnings from operations without considering firm ownership structure (debt/equity ratio) neither tax expenses. Then Operating Margin can also be analyzed when tracking ROA over time.

Both profit margin and operating margin are known as profitability ratios.

Now I will work with return on investment from the investors perspective -ROE. If I multiply ROE times TA and divide it by TA:

ROE_{t}=\frac{NI_{t}}{SHE_{t}}=\left(\frac{NI_{t}}{TA_{t}}\right)\left(\frac{TA_{t}}{SHE_{t}}\right)=ROA_{t}\left(\frac{TA_{t}}{SHE_{t}}\right)

Remembering that ROA is equal to Profit Margin times Asset Turnover:

ROE_{t}=\left(\frac{NI_{t}}{S_{t}}\right)\left(\frac{S_{t}}{TA_{t}}\right)\left(\frac{TA_{t}}{SHE_{t}}\right)

We can say that ROE is equal to Profit Margin times Asset Turnover times TA/SHE. \frac{TA_{t}}{SHE_{t}} is a measure of financial leverage, and is also known as equity multiplier. If the firm is not financially leveraged, meaning that debt is equal to zero, then the amount of SHE will be close to TA, so this ratio will closer to one (since SHE=TA-TL, and TL=Total debt+Current Liabilities). Then with this decomposition of ROE we could analyze why ROE changes over time at looking at profit margin, asset turnover and financial leverage. An interesting observation is that according to this formula, if the equity multiplier term increases, then ROE will increase. This means that if the firm leverages from debt with a decent interest rate, it is possible that the return on equity will improve. However, if interest rates are high, this will affect the profit margin ratio! Let’s go in more detail about financial leverage ratios.

2.9 Financial leverage ratios

Now, assuming that the firm has access to long-term debt, then:

TA_{t}=SHE_{t}+LTD_{t}+CL_{t}

This means that a company can finance its asset with either debt or equity. Now, we can do the following simple math to explore financial leverage ratios:

SHE_{t}=TA_{t}-\left(LTD_{t}+CL_{t}\right)

Now dividing all terms by the book value of shareholders’ equity:

\frac{TA_{t}}{SHE_{t}}=\frac{SHE_{t}+LTD_{t}+CL_{t}}{SHE_{t}}

Since total assets is equal to long-term debt plus current liabilities:

\frac{TA_{t}}{SHE_{t}}=1+\frac{TL_{t}}{SHE_{t}}

\frac{TL_{t}}{SHE_{t}} is a more direct measure of financial leverage: the more the LTD, the more financing, so this ratio increases, and also \frac{TA_{t}}{SHE_{t}} increases. So both are measures of financial leverage.

Other measures of financial leverage are the ratio of debt to equity and the ratio of debt to assets:

\frac{LTD_{t}}{SHE_{t}} = debt to equity ratio

\frac{LTD_{t}}{TA_{t}} = debt to assets ratio

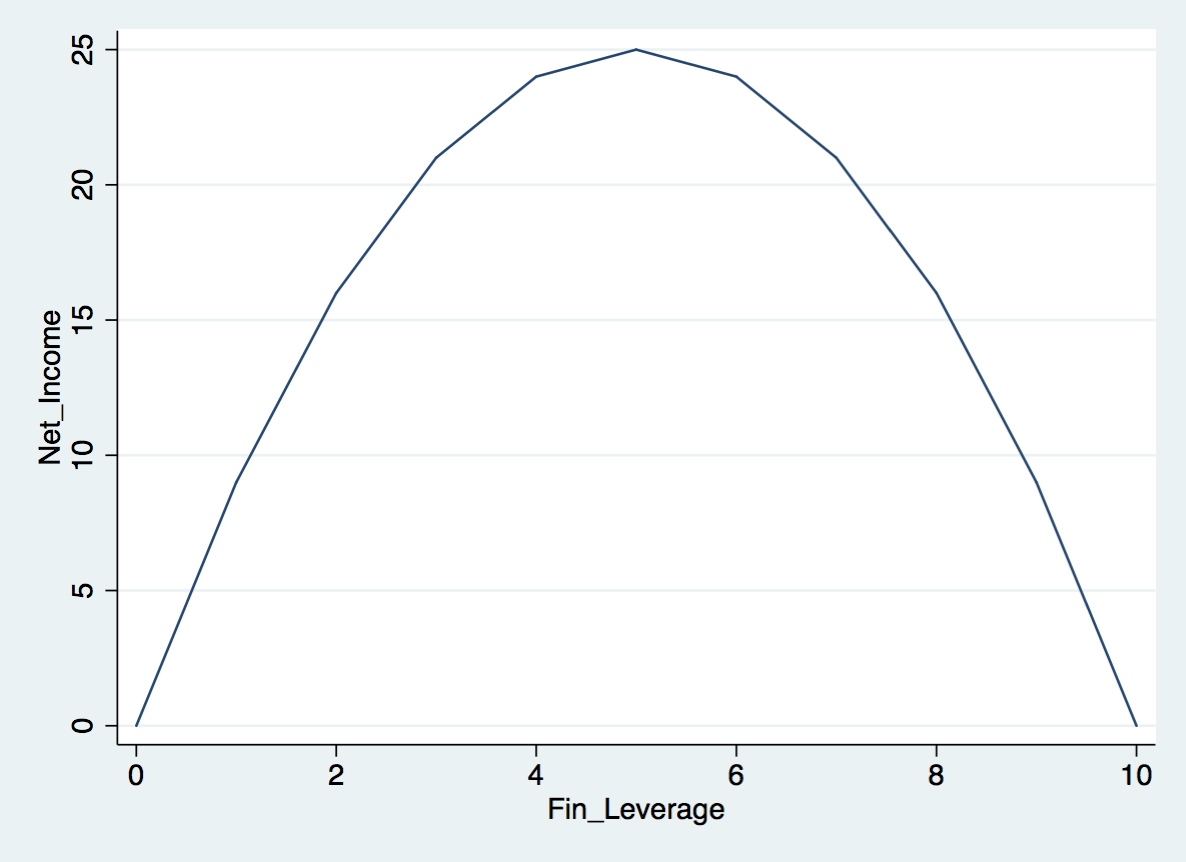

The interesting question is: what might be the best degree of financial leverage? It is difficult to find a right response to this question. It depends on many external -e.g. macroeconomic variables - and internal factors - e.g. cost of equity. However, financial leverage might have an inverse u-shaped effect on shareholders’ wealth. In other words, for each firm, there is an expected optimal point of leverage, where having more or less leverage than this optimal point might have a negative effect on shareholders’ wealth. Although not a perfect quadratic relation, for purpose of illustrating this inverse u-shaped relation, we can visualize the relation between financial leverage and net income something like:

Financing with debt obligates the company to pay principal and interest in a regular basis. However, equity financing does not obligate the company to be paying in specific periods. The board of directors and executives decide when and how much to pay as dividends. If the firm needs resources to grow, they can avoid paying dividends, but they cannot avoid paying debt. Then, getting financial debt always has its own risks besides the business risk of the company.

Looking at more detail about financial risk, we can analyze ratios related to interest expenses. Obviously the more the interest rate of a debt, the more the risk of the operation - in other words, the more the difficulty to make principal and interest payments. These ratios are also known as coverage ratios. Let’s see some of them.

\frac{EBIT_{t}}{IE_{t}}= Interest coverage ratio

As this ratio increases (interest expenses decrease), the company will have more better possibilities to pay its interest expenses.

This ratio does not consider other similar compromises of the company such as lease expenses. Lease expenses are similar to interest expenses in the sense that the company is obliged to make constant payments over a certain period. Since lease expenses are usually incorporated in EBIT as fixed costs, we can add them back and then compute the following ratio:

\frac{EBIT_{t}+LeaseExpenses_{t}}{IE_{t}+LeaseExpenses_{t}}= Fixed charge coverage ratio.

Usually this ratio is less than the interest coverage ratio and conveys a better picture of the ability of the company to comply with its finance compromises. This ratios conveys how many times the company can pay its debt and lease compromises from earnings.

Another important ratio related to the capability to pay interests is:

\frac{CashFlowfromOperations_{t}+IE_{t}+T_{t}}{IE_{t}}= Cash flow interest coverage ratio

Interest expenses and tax expenses are added back to Cash flow from operations to evaluate how many times the company can pay its interest expenses with its own resources generated by operations (cash flow from operations before interest and taxes). This is a better measure of the company’s ability to make its compromised payments since cash flow from operations is the actual cash the company has available. Then, why EBIT or earnings is not a good measure for looking at financial risk? The main reason comes from the difference between EBIT and cash flow. Cash flow from operations takes into account how much the firm is financing from suppliers (accounts payable), and also how much our customers are financing from us (accounts receivable). Besides this, EBIT considers the non-cash item depreciation as expense, where cash flow does not.

2.10 Liquidity ratios

Similar to financial leverage ratios that measure the company’s ability to meet long-term obligations, liquidity ratios measure the company’s ability to meet its short-term obligations but using not only cash but also those assets that can easily convert into cash. These assets are known as liquid assets or current assets or working capital. Then, subtracting current liabilities from current assets we can get the “net” working capital, which conveys the amount of resources needed for the day-to-day operations of the company’s long-term capital investment. Then if NWC = Net working capital:

NWC=CA-CL

Since net working capital is a measure of resources needed for day-to-day operations, then it is important to see the operating cycle of the company. Operating cycle refers to the time period that the company takes to generate cash flows from cash investment needed to produce goods or services. The operating cycle is usually composed of the following phases: a) purchase of raw material, b) produce goods and/or services, c) pay for inventory costs, d) sell goods and/or services, d) extend credit to customers through accounts receivable, and e) collecting cash from direct sales and from accounts receivable.

Then, if the company has a long operating cycle, then the company will need more net working capital to meet its day-to-day operations. Then, how can we measure the operating cycle of a company?

2.10.1 Operating cycle

As mentioned above, operating cycle refers to the time a company takes to produce goods, store them, sale them until the company collects cash from sales. In other words, operating cycle is the time it takes from investing cash into raw material and the time the company collects cash after producing goods, investing in inventory, selling them and collecting cash. This concept usually applies to manufacturing companies or commercial companies that hold inventory.

To provide an estimate of the operating cycle of the company we can think in two sub-cycles: 1) how long it takes to the company to sell 100% of its average inventory, and 2) how long it takes to the company - on average - to collect cash from sales. The first sub-cycle is also known as days sales in inventory, while the second sub-cycle is also known as the days of credit. This is a rough but acceptable estimate of the actual operating cycle. Then, let’s analyze these two sub-cycles.

2.10.2 Days sales in inventory

The inventory in the annual balance sheet represents the cost of goods “not” sold yet. Then, we can take this amount and divide it by the cost of good sold (COGS) at the end of the year. This will represent the proportion of goods that are not sold with respect to the goods sold during the year

\frac{Inventory_{t}}{COGS_{t}}= Proportion of goods not sold with respect to goods sold

Considering that these amounts are annual amounts, then we can translate this proportion in terms of the proportion of the year it takes to sell all the inventory if we assume that the company regularly produces and sells goods during the whole year, and also that the inventory level at the end of the year represents inventory levels during the year. Then, the number of days the company takes - on average - to sell all its inventory can be estimated by:

\frac{Inventory_{t}}{COGS_{t}}*365= Days sales in inventory=DSI

Now since most of the companies tend to select an end period with the lowest level of inventory during the year, this sub-cycle will be underestimated. It would be more accurate to calculate the average inventory of the last 4 quarters of the year instead of the last inventory of the year.

2.10.3 Days on credit

Days of credit is the average number of days the company takes to collect cash from sales. To easily estimate this sub-cycle we can assume that all sales are credit sales, but we do not have detailed information about how often our customers make their payments. However, we can estimate this by looking at accounts receivable. Then we can look at the proportion of accounts receivable with respect to credit sales - sales in this case. This proportion gives us a measure of how fast the company is collecting cash.

\frac{AR_{t}}{S_{t}}= Proportion of accounts receivable with respect to credit sales

Then, if we multiply this proportion by 365 we can get the average number of days the firm takes to collect cash from sales:

\frac{AR_{t}}{S_{t}}*365 = Days on credit=DOC

Now we can get the estimate of operating cycle by adding Days sales in inventory and Days on credit:

OperatingCycle=DSI+DOC=365*\left(\frac{Inventory_{t}}{COGS_{t}}+\frac{AR_{t}}{S_{t}}\right)

Once we have a proxy (measure) of the operating cycle, then we have an idea how long the company takes to generate cash from operations. This can help managers to decide which would be a good level of net working capital to make sure that the firm will not run out of cash and will not affect day-to-day operations. For example, if a company has an operating cycle of about 90 days, this means that it is strongly recommended to always have net working capital equivalent to cover 3 months of operations - including fixed and variable costs.

2.10.4 Cash conversion cycle

Now, considering that the company can take advantage of “free” financing from suppliers when buying on credit, then we can also estimate the an average number of days the company pays its accounts payable. If we put this credit cycle together with the operating cycle (subtracting credit cycle days from operating cycle days), we can get an estimate of number of days the company takes to convert or generate cash from operations considering not only the credit we give to our customers, but also the credit we get from our suppliers. This net cycle is known as cash conversion cycle (CCC).

To estimate the cash conversion cycle, we need to estimate the cycle for accounts payable, also know as days payable outstanding (DPO). We can follow the same logic we use to estimate the days on credit, assuming that all purchases are made on credit. Since we do not have detailed information about the value of all purchases and how much was on credit, we can use cost of good sold minus depreciation (of operating equipment) as the total value of credit purchase. Then, we can estimate the DPO as:

\frac{AP_{t}}{\left(COGS_{t}-DEP{}_{t}\right)}*365 = Days payable outstanding= DPODPO indicates how many days -on average- the company takes to pay its accounts payable. Then, if we subtract these days from the operating cycle, we can get a “net” cycle of cash generation known as Cash Conversion Cycle:

CCC=OperatingCycle-DPO=DSI+DOC-DPO

CCC=365*\left[\frac{Inventory_{t}}{COGS_{t}}+\frac{AR_{t}}{S_{t}}-\frac{AP_{t}}{\left(COGS_{t}-Depreciation_{t}\right)}\right]

The cash conversion cycle can also be used to establish minimum levels of net working capital - although operating cycle is a more conservative measure to use when deciding levels of liquidity or net working capital.

2.10.5 Liquidity ratios

Now I will mention liquidity ratios that conveys information about the ability of a company to meed its short-term obligations. These ratios are current ratio, quick ratio and net working capital-to-sales ratio.

\frac{CA_{t}}{CL_{t}}= Current ratioThis measure conveys the company’s ability to cover its current liabilities using its current assets. In theory, current assets can be converted into cash in no more than one year, so this measure might not be a good proxy of liquidity in the cases the company would need to quickly cover short-term obligations. Another more conservative measure of liquidity is the “quick” ratio. Since inventory might not be a quick asset to convert into cash, we subtract it from current assets:

\frac{CA_{t}-Inventory_{t}}{CL_{t}}=Quick ratioFinally, another measure of liquidity we can use is the net working capital-to-sales ratio, which measure the proportion of liquidity to total sales:

\frac{NWC_{t}}{S_{t}}= Net working capital-to-sales ratio

This ratio tells the company how many cents the company needs as net working capital for each dollar of sales. The longer the operating cycle, the bigger the net working capital and the bigger the net working capital-to-sales ratio.

With the days sales in inventory and days of credit we can have information about how liquid are inventory and accounts receivable, and which one is more liquid. With the liquidity ratios we can know the company’s ability to meet its short-term obligations with and without considering turning inventory into cash.

2.10.6 Activity ratios

Activity ratios measure the productivity of specific assets such as inventory, accounts receivable and total assets. It is measure in number of times the company turns over its assets. In other words, how many times a year or a quarter (the period depends on the type of financial statement used) the company moves or renew its assets.

Inventory turnover ratio

Inventory turnover ratio measures how many times a year or a quarter the company sells its inventory:

\frac{COGS_{t}}{Inventory_{t}}= Inventory turnover ratio

For example, if the inventory turnover ratio is equal to 3 times and we are using annual income statement, indicates that the company sells its inventory 3 times a year, on average. In other words, cash invested in inventory, and this inventory is sold 3 times a year. If we remember the Day sales in inventory ratio, the inventory turnover ratio is just 365 divided by the Day sales in inventory ratio. If the inventory turnover ratio is equal to 3 this means that the Day sales in inventory ratio is equal to 365/3, which is closer to 120 days.

2.10.7 Account receivable turnover

Accounts receivable turnover measures how many times a year the company collects its credit sales. Assuming that the accounts receivable at the end of the year is representative throughout the year, and assuming that 100% of the sales are on credit, then we can estimate the accounts receivable turnover dividing net credit sales by account receivable:

\frac{NetCreditSales_{t}}{AR_{t}}=Accounts receivable turnover ratio

NetCreditSales_{t}=S_{t}-SalesReturns_{t}

For example, if this ratio is equal to 15 times, then it means that the company collects cash from credit sales 15 times a year. This ratio indicates how effectively a company is using credit extended to customers. There is a risk of extending credit to customers since there is always the possibility of default (the fact that some credit sales will never be paid).

Looking at the “Days of credit” formula, we can see that Days of credit can be estimated just by dividing 365 by the accounts receivable turnover ratio (assuming that there is no Sales returns). In other words, if we consider 365 days in the year and the company collects cash from credit sales 15 times a year, this means that the company takes about 24 days (365/15) to collect cash from credit sales.

Total assets turnover

We had examined this ratio when we did the Du Pont analysis for return on assets. This ratio indicates how many times in the year the company generates the total amount of assets with sales:

\frac{S_{t}}{TA_{t}}=Total asset turnover (ATO)This ratio is a measure of efficiency and effectiveness of asset usage. The higher the asset turnover the more efficient and effective the usage of assets to generate sales. It is also possible to use other type of asset as denominator in case we want to evaluate the efficiency of fixed and/or equipment assets in the case of manufacturing companies. For example, if we replace Total Assets by Fixed assets we get the fixed asset turnover ratio, which measure the efficiency and effectiveness of the company’s fixed-assets without considering other assets such as intangible assets or current assets.

Common-size analysis

Common-size analysis is used to examine proportions in two financial statements: balance sheet and income statement. The “vertical” common-size analysis uses total assets as the benchmark, so all items of the balance sheet are expressed in percentage of total assets. In the case of income statements the benchmark is total sales, so all items in the income statement are expressed in percentage of total sales.

The “horizontal” common-size analysis in both the balance sheet and income statement use amounts of previous years for each item as benchmark, so all items will be expressed in percentages of last-period(s) items.

Common-size analysis is very useful when comparing the company with other companies since percentages are comparable across any company. This analysis provides a quick look of financial condition and business performance of the company, while financial ratios provide more detail information about the financial condition and operational efficiency of the company.

2.11 Final remark

This is a brief chapter about financial analysis. There are tons of accounting and finance books about financial analysis and financial accounting that cover financial ratios in more detail. However, these basic ratios are the most used in the real world. A financial professional must understand how these ratios are calculated, the reason of using them, and practical application of the ratios to come up with a concise financial perspective of any company at any time and over time. A good financial manager is able to estimate and come up with many of combinations of financial items to get financial ratios, but the most important skill of a financial manager is to interpret financial statements and financial ratios, and be able to compare companies with other companies and with its own company over time.

I downloaded Amazon financial information from the SEC-EDGAR online database (https://www.sec.gov/edgar.shtml).↩︎